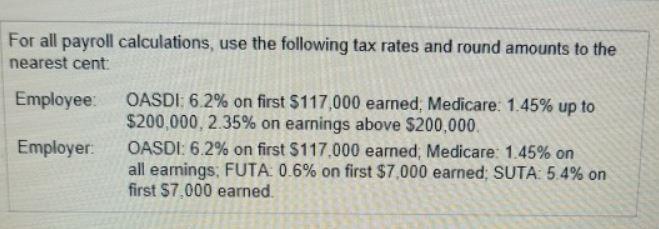

Liam Wallace is general manager of moonwalk salons. during 2016 while this works for the company all year at a $13600 monthly salary he also earned a year end bonus = 15% of his annual salary. Wallace's federal income tax withheld during 2016 was $952 per month plus $3672 on his bonus check. state income tax withheld came to a $150 per month plus $90 on bonuses. FICA tax was withheld on annual earnings. Wallace authorized the following payroll deductions charity fund contribution of 3% of total earnings and life insurance of $50 per month.

1. Compute Wallace's gross pay, payroll deductions, and net pay for the full year 2016. Round all amounts to the nearest dollar

2. Compute Moonwalk's total 2016 payroll expense for Wallace

3. Make the journal entry to record Moonwalk's expense for Wallace's total earnings for the year, his payroll deductions, and net pay. Debit Salaries Expense and Bonus Expense as appropriate. Credit liability accounts for the payroll deductions and Cash for net pay. An explanation is not required

4. Make the journal entry to record the accrual of Moonwalk's payroll tax expense for Wallace's total earnings.

Answers

Answer:

1. Gross Pay = Salary + Bonus

= (13,600 * 12) + (15% * (13,600 * 12))

= 163,200 + 24,480

= $187,680

2.Wallace 2016 Payroll = Gross Pay - Deductions

Deductions

= FICA-Social security tax + FICA-Medicare tax + Federal income tax + State income tax + Charity Fund contribution + Life insurance contribution

= (6.2% x 117,000) + (1.45% x 187,680) + {(952 x 12) + 3,672} + {(150 x 12) + 90} + (3% x 187,680) + (50 x 12)

= 7,254 + 2,721.36 + 15,096 + 1,890 + 5,630.40 + 600

= $33,191.76

Wallace 2016 Payroll = 187,680 - 33,191.76

= $154,488.24

3.

DR Salaries Expense 163,200

Bonus Expense 24,480

CR FICA-Social Security Tax Payable 7,254

FICA- Medicare Tax Payable 2,721.36

Federal Income tax payable 15,096

State Income tax payable 1,890

Charity Fund Payable 5,630.90

Life Insurance Payable 600

Cash 154,488.24

4. Moonwalk's payroll tax expense for Wallace's total earnings.

DR Payroll Tax Expense 10,395.36

CR FICA-Social Security Tax Payable 7,254

FICA- Medicare Tax Payable 2,721.36

FUTA Payable (0.6% * 7,000) 42

SUTA Payable ( 5.4% * 7,000) 378

Related Questions

A Corporation has two divisions: the South Division and the West Division. The corporation's net operating income is $26,900. The South Division's divisional segment margin is $42,800 and the West Division's divisional segment margin is $29,900. What is the amount of the common fixed expense not traceable to the individual divisions

Answers

Answer:

$45,800

Explanation:

Common fixed expense not traceable to the individual divisions = South division's divisional segment margin + west division's divisional segment - corporation's net operating income

Common fixed expense not traceable to the individual divisions = $42,800 + $29,900 - $26,900

Common fixed expense not traceable to the individual divisions = $45,800

The given statements pertain to aggregate supply and aggregate demand. Label each statement as being either true or false.

Statement 1: An increase in the cost of energy affects both aggregate supply and aggregate demand.

A. True

B. False

Statement 2: One of the factors that increase aggregate demand is the consumption of more imports.

A. True

B. False

Statement 3: If the value of people's stock portfolios increases or if peoples houses appreciate in value, then this very easily could lead to an increase in aggregated demand.

A. True

B. False

Answers

Answer:

Statement 1: An increase in the cost of energy affects both aggregate supply and aggregate demand.

A. TrueAn increase in energy costs reduces both aggregate supply and demand.

Statement 2: One of the factors that increase aggregate demand is the consumption of more imports.

B. FalseIf net exports decrease (exports - imports), then the aggregate demand curve will shift to the left, which means it will decrease.

Statement 3: If the value of people's stock portfolios increases or if peoples houses appreciate in value, then this very easily could lead to an increase in aggregated demand.

A. TrueThis would lead to an increase in the net worth of households, which generally leads to higher spending.

Broca Corporation has a current ratio of 2.5. Which of the following transactions will increase Broca's current ratio? Select one: a. the purchase of inventory for cash. b. the collection of an account receivable. c. the payment of an account payable. d. none of the above.

Answers

Answer:

b. the collection of an account receivable

Explanation:

The formula to compute the current ratio is shown below:

As we know that

Current ratio = Current assets ÷ Current liabilities

If the current ratio is 2.5 that means the current assets is higher than the current ratio

As per the given options, the option b is correct and hence the same is to be considered

The transaction that will increase Broca's current ratio is d. none of the above.

The current ratio is not increased by the purchase of inventory for cash because this transaction has no effect on the current assets. The collection of an account receivable is not going to increase the current ratio for the same reason above (no effect on the current assets).

The payment of an account payable reduces the current assets and current liabilities by the same amount and will not affect the current ratio.

Thus, the transaction that will increase the current ratio is d.

Learn more: https://brainly.com/question/17189534

Adelberg Corporation makes two products: Product A and Product B. Annual production and sales are 1,500 units of Product A and 1,500 units of Product B. The company has traditionally used direct labor-hours as the basis for applying all manufacturing overhead to products. Product A requires 0.4 direct labor-hours per unit and Product B requires 0.2 direct labor-hours per unit. The total estimated overhead for next period is $87,630. The company is considering switching to an activity-based costing system for the purpose of computing unit product costs for external reports. The new activity-based costing system would have three overhead activity cost pools--Activity 1, Activity 2, and General Factory--with estimated overhead costs and expected activity as follows:

Expected Activity

Activity Cost Pool Estimated Overhead Costs Product A Product B Total

Activity 1 $ 41,400 1,000 500 1,500

Activity 2 15,720 800 400 1,200

General Factory 30,510 600 300 900

Total $ 87,630

(Note: The General Factory activity cost pool's costs are allocated on the basis of direct labor-hours.)

The overhead cost per unit of Product B under the activity-based costing system is closest to:_________

a. $42.90

b. $9.10

c. $21.30

d. $63.92

Answers

Answer:

Results are below.

Explanation:

First, we need to calculate the predetermined overhead rate for each activity:

Predetermined manufacturing overhead rate= total estimated overhead costs for the period/ total amount of allocation base

Activity 1= 41,400/1,500= $27.6 per unit of activity

Activity 2= 15,720/1,200= $13.1 per unit of activity

General Factory= 30,510/900= $33.9 per direct labor hour

Now, we can allocate overhead to product B:

Allocated MOH= Estimated manufacturing overhead rate* Actual amount of allocation base

Activity 1= 27.6*500= $13,800

Activity 2= 13.1*400= $5,240

General Factory= 33.9*300= $10,170

Total allocated overhead= $29,210

Unitary allocated overhead= 29,210/1,500= $19.47

Wilson Products uses standard costing. It allocates manufacturing overhead (both variable and fixed) to products on the basis of standard direct manufacturing labor-hours (DLH). Wilson Products develops its manufacturing overhead rate from the current annual budget. The manufacturing overhead budget for 2014 is based on budgeted output of 672,000 units, requiring 3,360,000 DLH. The company is able to schedule production uniformly throughout the year.

A total of 72,000 output units requiring 321,000 DLH was produced during May 2014. Manufacturing overhead (MOH) costs incurred for May amounted to $ 355,800. The actual costs, compared with the annual budget and 1/12 of the annual budget, are as follows:

Calculate the following amounts for Wilson Products for May 2014:

Total Amount Per Output Unit Per DLH Input Unit Monthly MOH Budget May 2017 Actual MOH Costs for May 2017

Variable MOH

Indirect manufacturing labor $1,008,000 $1.50 $0.30 $84,000 $84,000

Supplies 672,000 1.00 0.2 56,000 117,000

Fixed MOH

Supervision 571,200 0.85 0.17 47,600 41,000

Utilities 369,600 0.55 0.11 30,800 55,000

Depreciation 705,600 1.05 0.21 58,800 88,800

Total $33,26,400 $4.95 $0.99 $277,200 $355,800

Required:

a. Total manufacturing overhead costs allocated.

b. Variable manufacturing overhead spending variance.

c. Fixed manufacturing overhead spending variance.

d. Variable manufacturing overhead efficiency variance.

e. Production-volume variance Be sure to identify each variance as favorable (F) or unfavorable(U).

Answers

Answer:

Please see attached solution

Explanation:

a. Total manufacturing overhead costs allocated $356,400

b. Variable manufacturing overhead spending variance $40,500U

c. Fixed manufacturing overhead spending variance $17,600U

d. Variable manufacturing overhead efficiency variance $19,500F

e. Production volume variance $39,200F

Please find attached detailed solution to the above questions

So you want to finance a car for $4,840. Let’s say we offer you a 4.5% interest rate on a 2-year loan and 6% on a 5-year loan. Enter this info into the calculator to see your monthly and total cost by loan term.

Financing Amount

$4840

Correct

Interest Rate on 2-Year Loan

Interest Rate on 5-Year Loan

Answers

Answer:

Interest Rate on 2-Year Loan...$435.6

Interest Rate on 5-Year Loan...$1,452

Explanation:

The formula for calculating simple interest is as follows.

I = P x R x T,

where I = interest

P= Principal

R= interest rate

T= time

For the loan at 4.5 percent for 2 years, the interest will be

= $4,840 x 4.5/100 x 2

= $4,840 x 0.045 x 2

= $435.6

Total cost of the loan will principal plus interest

=$435.6 + $4,840

=$5,275.6

Monthly loan cost

= $5,275.6/24

=$219.81

Total loan cost..$5,275.6

Monthly loan cost ...$219.81

For the Loan at 6 percent for 5 years, the interest will be

= $4,840 x 6/100 x 5

= $4,840 x 0.06 x 5

=$1,452

Total cost of the loan will be principal plus interest

=$ 4,840 + $1,452

=$6,292

Monthly costs will be

=$6,292/60

=$104.87

Total loan cost... $6,292

Monthly loan costs... $104.87

Which best describes the role that government and business play in investments?

O They both use taxes to support a country's growth.

They both invest money to earn a profit.

They both receive capital to use for growth.

They both act as angel investors for start-ups.

Answers

Answer:

They both receive capital to use for growth.

Explanation:

The government received the capital in the form of tax that being paid by the citizens. After collecting the tax income, the government allocated it to make a couple of investments such as building the country's infrastructure, providing aid for people to pursue education, and investing in scientific research/development.

Business on the other hand could receive their capital from either reallocating their profit or receiving capital injection from the investors. They use the capital for growth by reinvesting it to increase the scope of their business operation or putting it under investment accounts.

Statement that best describes the role that government and business play in investments is They both receive capital to use for growth

What is an investment?Investment can be regarded as the input that is been put into some business in order to generate revenue.

however, this also applies to the government because they use the public funds as investment for the betterment of the economy and the public.

Learn more about investments at;

https://brainly.com/question/200850

A University is offering a charitable gift program. A former student who is now 50 years old is consider the following offer: The student can invest $8,900.00 today and then will be paid a 9.00% APR return starting on his 65th birthday (i.e For a $10,000 investment, a 9% rate would mean $900 per year). The program will pay the cash flow for this investment while you are still alive. You anticipate living 21.00 more years after your 65th birthday. The former student wants a return of 6.00% on his investments, but would like to consider this opportunity.

Required:

Using the student's desired return, what is the value of this deferred annuity today on his 50th birthday?

Answers

Answer:

The value of this deferred annuity today on his 50th birthday is $2,621.27.

Explanation:

Since the student's desired return of 6% will also start to be paid starting on his 65th birthday, the value of this deferred annuity today on his 50th birthday can be calculated by first calculating the value of the investment on the 65th birthday.

We therefore proceed with the following two steps:

Step 1: Calculation of the value of the investment on the 65th birthday

The value of the investment on the 65th birthday can be calculated using the formula for calculating the present value of an ordinary annuity as follows:

PV = P * ((1 - (1 / (1 + r))^n) / r) …………………………………. (1)

Where;

PV at 65 = Present value of the annuity at 65th birthday =?

P = Annuity payment = Invested amount * Student's desired return = $8,900 * 6% = $534

r = Student's desired return rate = 6%, or 0.06

n = number of more years anticipate to live after 65th birthday = 21

Substitute the values into equation (1) to have:

PV at 65 = $534 * ((1 - (1 / (1 + 0.06))^21) / 0.06)

PV at 65 = $534 * 11.764076621288

PV at 65 = $6,282.02

Therefore, the value of the investment on the 65th birthday is $6,282.02.

Step 2: Calculation of the value of this deferred annuity today on his 50th birthday

The value of this deferred annuity today on his 50th birthday can therefore be calculated using the simple present value for as follows:

PV at 50 = PV at 65 / (1 + r)^N …………………………….. (2)

Where;

PV at 50 = the value of this deferred annuity today on his 50th birthday = ?

PV at 65 = Present value of the annuity at 65th birthday = $6,282.02

r = Student's desired return rate = 6%, or 0.06

N = number of years from 50th birthday to 65th birthday = 65 - 50 = 15

Substitute the values into equation (2) to have:

PV at 50 = $6,282.02 / (1 + 0.06)^15

PV at 50 = $6,282.02 / 2.39655819309969

PV at 50 = $2,621.27

Therefore, the value of this deferred annuity today on his 50th birthday is $2,621.27.

The revenues budget identifies: a. expected cash flows for each product b. actual sales from last year for each product c. the expected level of sales for the company d. the variance of sales from actual for each product

Answers

Answer:

c. the expected level of sales for the company

Explanation:

Revenue/Sales Budget is the first budget to be prepared by most companies because most businesses are sales led.

This Budget shows, the expected level of sales for the company.

It is important that marketers be able to identify which strategy a competitor is using so that they better understand how to position their own products and services. You will see a list of recent or potential strategic decisions made by large firms, and your job is to identify which type of strategy was used in each example.

While there are a variety of strategies across industries, most fall under four basic categories.

1. Market penetration strategies emphasize selling more existing products and services to existing customers.

2. Product development strategies involve creating new goods or services for existing markets.

3. Market development strategies focus on selling existing products or services to new customers. The targeted new customers could be a different gender, age group, or international market.

4. Finally, diversification strategies involve offering new products that are unrelated to the existing products produced by the organization.

Select the most appropriate category of emotional intelligence for below mention behaviors.

i. Arm and Hammer selling baking soda for new purposes.

a. Market penetration

b. Product development

c. Market development

d. Diversification

ii. Apple opening mini-stores within Target

a. Market penetration

b. Product development

c. Market development

d. Diversification

iii. Disney purchasing ESPN

a. Market penetration

b. Product development

c. Market development

d. Diversification

Answers

Answer:

1. Market development

2. Market penetration

3. Diversification

Explanation:

we have already been given a definition of these concepts from question

1.

for Ann and hammer: it is market development because they are trying to create a product for new purposes

2.

for apple: since they are opening mini stores within target they are trying to have an expansion approach where more products and services would be sold to their customers.

3.

for disney: they are diversifying into a new product entirely. ESPN is a well known channel for sporting related activities.

Chance company had two operating divisions, one manufacturing farm equipment and other office supplies. Both divisions are considered separate components as defined by generally accepted accounting principles. The farm equipment component had been unprofitable, and on Sept. 1, 2016, the company adopted a plan to sell the assets of the division.

The actual sale was completed on Dec. 15, 2016, at the price of $600,000. The book value of the division's assets was $1,000,000, resulting in a before-tax loss of $400,000 on the sale. The division incurred a before-tax operating loss from operations of $130,000 from the beginning of the year through Dec. 15. The income tax rate is 40%. Chances after-tax income from its continuing operations is $350,000.

Required:

Prepare an income statement for 2016 beginning with income from continuing operations. Include appropriate EPS disclosures assuming that 100,000 shares of common stock were outstanding throughout the year.

Answers

Answer:

-21,000

Explanation:

We can calculate the net income by Adding/deducting the gain/loss on the discontinued operations from the gain/loss of the continuing operations.

INCOME STATEMENT

Income from continuing Operations $350,000

Discontinued Operations

Loss from discontinued operations(w) -530,000

Income tax benefit $159,000

(400,000+130,000) x 30%

Net Income -21,000

Earning per share

Continuing Operations $3.5

(350,000/100,000)

Discontinued Operations -$5.3

(-530,000/100,000)

Net Income -$1.8

Working

Sale value of the segment $600,000

Book value of the segment ($1,000,000)

loss on sale of segment -$400,000

Loss from the Operations of the segment -$130,000

Loss on discontinued operation -$530,000

The City of Waterville applied for a grant from the state government to build a pedestrian bridge over the river inside the city’s park. On May 1, the city was notified that it had been awarded a grant of up to $200,000 for the project. The state will provide reimbursement for allowable expenditures. On May 5, the special revenue fund entered into a short-term loan with the General Fund for $200,000 so it could start bridge construction. During the year, the special revenue fund expended $165,000 for allowable bridge construction costs, for which it submitted documentation to the state. Reimbursement was received from the state on December 13, 2017.

Required:

For the special revenue fund, provide the appropriate journal entries, if any, that would be made for the following.

a. May 5, 2017, loan from General Fund.

b. During FY 2017, bridge expenditures and submission of reimbursement documentation.

c. December 13, 2017, receipt of the grant reimbursement funds.

d. December 31, 2017, adjusting and closing entries.

Answers

Answer:

The City of Waterville

a. May 5:

Debit Cash $200,000

Credit InterFund Loan Payable $200,000

To record the loan from the general fund.

b. Debit Bridge Expenditure $165,000

Credit Vouchers Payable $165,000

To record the bridge expenditure for the year.

Debit Grant Receivable from State $165,000

Credit Grant Revenue $165,000

To record the submission of documentation for reimbursement.

c. Debit Cash $165,000

Credit Grant Receivable from State $165,000

To record the receipt of grant reimbursement.

d. Debit Revenues $165,000

Credit Expenditures $165,000

To record the revenues received and the expenditures.

Explanation:

The City of Waterville's application does not attract any journal entries. No journal entries are also made on May 1 when the city was notified of the grant award. Journal records are made from May 5 when the short-term loan arrangement was concluded with the General Fund.

The following inventory valuation errors have been discovered for Knox Corporation:

The 2015 year-end inventory was overstated by $23,000

The 2016 year-end inventory was understated by $61,000

The 2017 year-end inventory was understated by $17,000

The reported income before taxes for Knox was:

Year: Income before Taxes:

2015 $138,000

2016 $254,000

2017 $168,000

Required:

Compute what income before taxes for 2015, 2016, and 2017 should have been after correcting for the errors.

Answers

Answer:

Income +/- inventory adjustment

2015: 138,000 - 23,000 = 115,000

2016: 254,000 + 61,000 = 315,000

2017: 168,000 + 17,000 = 185,000

Explanation:

Inventory Identity:

Beginning + Purchases = Ending + COGS

As the mistake is on the right side it compensates by the other component which is COGS

When the inventory is overstated this means COGS is understated.

We didn't record the cost of good sold thefore our gross profit is higher making the net income higher.

When the inventory is understated this means COGS is overstated.

We record more cost of goods sold thefore our gross profit is lower making the net income fewer as well.

An Investment Adviser Representative (IAR) manages the assets of the ABC Corporation Profit Sharing Plan. The trustee of the plan contacts the IAR, explaining to the IAR that he wants a check drawn from the plan account to buy a building that ABC Corporation will occupy. The IAR should:

Answers

Answer:

refuse to issue the check because it is a breach of the IAR's fiduciary obligation

Explanation:

This check should not be issued because if it is issued it would be a breach of the investment advisor representative fiduciary obligation. His main responsibility is to offer advices that relates to investment because he is a financial planner. He has to act in the best interest of his client with loyalty and also in good faith.

KW Steel Corp. uses the LIFO method of inventory valuation. Waretown Steel, KW’s major competitor, instead uses the FIFO method. The following are excerpts from each company’s 20X1 financial statements:

KW Steel Corp. Waretown Steel ($ in millions)

20X1 20X0 20X1 20X0

Balance sheet inventories $797.6 $692.7 $708.2 $688.6

LIFO reserve 378.0 334.9

Sales 4,284.8 4,029.7 3,584.2 3,355.8

Cost of goods sold 3,427.8 3,226.5 2,724.0 2,617.5

Required:

a. Compute each company’s 20X1 gross margin percentage and inventory turnover using cost of goods sold as reported by each company. Restate KW’s cost of goods sold and inventory balances to the FIFO basis. On the basis of its adjusted data, recompute KW’s gross margin percentage and inventory turnover.

b. Restate KW's cost of goods sold and inventory balances to the FIFO basis. On the basis of its adjusted data, re-compute KW's gross margin percentage and inventory turnover. Explain how the revised figures alter your earlier comparisons.

Answers

Answer:

KW Steel Corp. and Waretown Steel

LIFO and FIFO Inventory Valuation Methods:

a. Computation of each company's 20X1 gross margin percentage and inventory turnover:

KW Steel Corp. Waretown Steel

($ in millions) ($ in millions)

20X1 20X0 20X1 20X0

B/sheet inventories $797.6 $692.7 $708.2 $688.6

LIFO reserve 378.0 334.9

Sales 4,284.8 4,029.7 3,584.2 3,355.8

Cost of goods sold 3,427.8 3,226.5 2,724.0 2,617.5

Gross margin $857.0 $803.2 $860.0 $738.3

Gross margin % 20% 24%

Average Inventory = $745.15 $698.4

Inventory Turnover 4.6 ($3,427.8/$745.15) 3.9 ($2,724.0/$698.4)

b. Restatement of KW's cost of goods sold and inventory balances to FIFO:

KW Steel Corp. Waretown Steel

($ in millions) ($ in millions)

20X1 20X0 20X1 20X0

Sales 4,284.8 4,029.7 3,584.2 3,355.8

Cost of goods sold $3,805.8 $3,561.40

Gross margin $479.0 $468.3 $860.0 $738.3

Gross margin % 11.2% 24%

Inventory Turnover 9.8 ($3,805.8/$388.75) 3.9 ($2,724.0/$698.4)

c. The performance of KW Steel worsened with the reinstatement of the LIFO reserves. Before the reinstatement, KW Steel was running closely behind its competitor, Waretown Steel. But after the reinstatement, Waretown gave KW Steel more gap in performance. This reinstatement shows that when the performances of two companies are compared based on different criteria, the financial analyst will likely arrive at a wrong conclusion.

Explanation:

a) Data and Calculations:

KW Steel Corp. Waretown Steel

($ in millions) ($ in millions)

20X1 20X0 20X1 20X0

B/sheet inventories $797.6 $692.7 $708.2 $688.6

LIFO reserve 378.0 334.9

Sales 4,284.8 4,029.7 3,584.2 3,355.8

Cost of goods sold 3,427.8 3,226.5 2,724.0 2,617.5

Gross margin $857.0 $803.2 $860.0 $738.3

Gross margin % 20% 24%

Average Inventory = $745.15 $698.4

Inventory Turnover 4.6 ($3,427.8/$745.15) 3.9 ($2,724.0/$698.4)

c.

KW Steel Corp. Waretown Steel

($ in millions) ($ in millions)

20X1 20X0 20X1 20X0

B/sheet inventories $797.6 $692.7 $708.2 $688.6

LIFO reserve 378.0 334.9

FIFO balance $419.6 $357.8

Cost of goods sold 3,427.8 3,226.5 2,724.0 2,617.5

LIFO reserve 378.0 334.9

Average Inventory = $745.15 $698.4

New Average Invt. 388.75

Here are comparative statement data for Crane Company and Sheridan Company, two competitors. All balance sheet data are as of December 31, 2017, and December 31, 2016.

Crane Company Sheridan Company

2017 2016 2017 2016

Net sales $1,855,000 $596,000

Cost of goods sold 1,063,000 291,000

Operating expenses 265,000 89,000

Interest expense 8,600 3,200

Income tax expense 74,900 35,000

Current assets 534,599 $512,352 136,671 $130,326

Plant assets (net) 863,952 820,000 229,154 206,332

Current liabilities 08,773 124,337 57,971 49,661

Long-term liabilities 186,944 147,600 48,577 41,000

Common stock, $10 par 820,000 820,000 196,800 196,800

Retained earnings 282,834 240,416 62,477 49,197

Prepare a vertical analysis of the 2017 income statement data for Crane Company and Sheridan Company.

Answers

Answer:

Please see attached.

Explanation:

Please see attached vertical analysis of the 2017 income statement data for Crane company and Sheridan company.

Note: The percent for each company - Crane and Sheridan is arrived at by dividing each item( expense or income) by sales multiplied by 100.

For instance for Crane, the percentage for Gross profit is = ($792,000 / $1,855,000 ) × 100

= 42.7%

Crow earned $585.15 during the week ended March 1, 20--. Prior to payday, Crow had cumulative gross earnings of $4,733.20. Round your answers to the nearest cent. a. The amount of OASDI taxes to withhold from Crow's pay is $ . b. The amount of HI taxes to withhold from Crow's pay is

Answers

Answer:

A. $36.28

B. $8.48

Explanation:

a. Calculation for the amount of OASDI taxes to withhold from Crow's pay

OASDI taxes is 6.2%

Hence,

OASDI taxes to withhold = 585.15*0.62

OASDI taxes to withhold = $36.28

Therefore the OASDI taxes to withhold from Crow's pay is $36.28

b. Calculation for the amount of HI taxes to withhold from Crow's pay

HI taxes is 1.45%

Hence,

HI taxes to withhold =585.15*0.0145

HI taxes to withhold=$8.48

Therefore HI taxes to withhold from Crow's pay is $8.48

Presented below are condensed financial statements adapted from those of two actual companies competing as the primary players in a specialty area of the food manufacturing and distribution industry. ($ in millions, except per share amounts.)

Balance Sheets

Metropolitan Republic

Assets $ 179.3 $ 37.1

Cash

Accounts receivable (net) 422.7 325.0

Short-term investments — 4.7

Inventories 466.4 635.2

Prepaid expenses and other current assets134.6 476.7

Current assets $ 1,203.0 1,478.7

Property, plant, and equipment (net) 2,608.2 2,064.6

Intangibles and other assets 210.3 464.7

Total assets $ 4,021.5 $4,008.0

Liabilities and Shareholders’ Equity

Accounts payable $ 467.9 691.2

Short-term notes 227.1 557.4

Accruals and other current liabilities 585.2 538.5

Current liabilities $ 1,280.2 1,787.1

Long-term debt 535.6 542.3

Deferred tax liability 384.6 610.7

Other long-term liabilities 104.0 95.1

Total liabilities $ 2,304.4 3,035.2

Common stock (par and additional paid-in capital)

144.9 335.0

Retained earnings 2,476.9 1,601.9

Less: treasury stock (904.7) (964.1)

Total liabilities and shareholders’ equity $

4,021.5 4,008.0

Income Statements

Net sales 5,698.0 7,768.2

Cost of goods sold (2,909.0) (4,481.7)

Gross profit $ 2,789.0 3,286.5

Operating expenses (1,743.7 ) (2,539.2)

Interest expense (56.8) (46.6)

Income before taxes $ 988.5 700.7

Tax expense (394.7) (276.1)

Net income 593.8 424.6

Net income per share $ 2.40 6.50

Note: Because comparative statements are not provided you should use year-end balances in place of average balances as appropriate.

Required:

Calculate the rate of return on assets for the following companies

Calculate the return on assets for both companies.

Calculate the Rate of return on shareholders’ equity for the following companies

Calculate the equity multiplier for the following companies.

Calculate the acid-test ratio and current ratio for the following companies.

Calculate the receivables and inventory turnover ratios the following companies.

Calculate the times interest earned ratio for the following companies.

Answers

Answer and Explanation:

We refer to balance sheet figures for each company stated above to retrieve figures for our calculations and use the following formulas for calculations:

For return on assets= net imcome/total assets

For rate of return on shareholders equity =net income/equity

For equity multiplier= total assets/ total equity

For acid-test ratio=liquid assets/current liabilities

For current ratio =current assets/current liabilities

For receivables = credit sales /acct receivables and inventory turnover ratios=cost of goods/inventory

For times interest earned ratio=ebit/interest expenses

The following are selected account balances from Penske Company and Stanza Corporation as of December 31, 2021:

Penske Stanza

Revenues $(842,000 ) $(568,000 )

Cost of goods sold 299,700 142,000

Depreciation expense 207,000 304,000

Investment income Not given 0

Dividends declared 80,000 60,000

Retained earnings, 1/1/21 (668,000 ) (222,000 )

Current assets 572,000 566,000

Copyrights 1,076,000 449,500

Royalty agreements 604,000 1,180,000

Investment in Stanza Not given 0

Liabilities (546,000 ) (1,631,500 )

Common stock (600,000 )($20 par) (200,000 ) ($10 par)

Additional paid-in capital 150,000 80,000

On January 1, 2013, Penske acquired all of Stanza's outstanding stock for $680,000 fair value in cash and common stock. Penske also paid $10,000 in stock issuance costs. At the date of acquisition copyrights (with a six-year remaining life) have a $440,000 book value but a fair value of $560,000.

a. As of December 31,2013, what is the consolidated copyrights balance?

b. For the year ending December 31,2013, what is consolidated net income?

c. As of December 31,2013, what is the consolidated retained earnings balance?

d. As of December 31,2013, what is the consolidated balance to be reported for goodwill?

Answers

Answer:

a. $1,625,500

b. $437,300

c. $1,025,300

d. $58,000

Explanation:

a. As of 31, December 2013, what is the consolidated copy rights balance

b. For the year ending, December 31, 2013, what is consolidated net income

c. As of December 31, 2013, what is the consolidates retained earnings balance

d. As of December 31, 2013 what is the consolidated balance to be reported for Goodwill.

Please find attached detailed explanations to the above questions and answers.

In 1998, the Russian government defaulted on its bonds. According to the open-economy macroeconomic model, this should have

Answers

Answer:

An increase in the net export and Russian interest rate.

Explanation: An open economy is an economy where all players which includes traders, investors and other stakeholders in the economy both within and outside the economy freely conduct their businesses and are controlled by market forces with minimal interference by Government agencies.

According to the open-economy macroeconomic model with the defaulting by the Russian government in 1998 will definitely lead to an increase in net export and an increase in Russian Interest rate.

What will be the nominal rate of return on a perpetual preferred stock with a $100 par value, a stated dividend of 8% of par, and a current market price of (a) $62, (b) $81, (c) $97, and (d) $136

Answers

Answer and Explanation:

The computation of the risk premium is shown below:-

Rate of return = Dividend ÷ Current market price of preferred stock

The dividend should be

= $100 × 8%

= $8

a Rate of return = $8 ÷ $62

= 12.90%

b. Rate of return = $8 ÷ $81

= 9.88%

c. Rate of return = $8 ÷ $97

= 8.25%

d. Rate of return = $8 ÷ $136

= 5.88%

On July 1, 2020, Buffalo Inc. made two sales.

1. It sold land having a fair value of $904,290 in exchange for a 4-year zero-interest-bearing promissory note in the face amount of $1,422,914. The land is carried on Buffalo's books at a cost of $591,300.

2. It rendered services in exchange for a 3%, 8-year promissory note having a face value of $408,830 (interest payable annually).

Buffalo Inc. recently had to pay 8% interest for money that it borrowed from British National Bank. The customers in these two transactions have credit ratings that require them to borrow money at 12% interest.

Required:

Record the two journal entries that should be recorded by Vaughn Inc. for the sales transactions above that took place on July 1, 2020.

Answers

Answer:

Journal 1

July 1

Note Receivable $1,422,914 (debit)

Profit and Loss $851,614 (credit)

Land $591,300 (credit)

Sale of land on credit

Journal 2

July 1

Note Receivable $861,394 (debit)

Service Revenue $861,394 (credit)

Rendered Services on credit

Explanation:

Journal 1

Sale of land on credit :

De-recognise the Land in Buffalo Inc. books at cost, Recognise the Assets of Note Receivable and a Profit from sale. Proceeds are measured at the future value

Future Value :

PV = $1,422,914

n = 4

pmt = $0

p/yr = 1

fv = ?

Using a financial calculator the future value is $1,422,914.

Journal 2

Rendered Services on credit :

Recognize the Assets of Note Receivable and Recognise the Revenue at the future value.

Future Value :

pv = - $408,830

n = 8

pmt = 3% × $408,830 = $12,264.90

i = 12%

p/yr = 1

fv = ?

Using a financial calculator, the future value is $861,394

Shake Shack Inc. reports the following items in its 2015 statement of cash flow. For each item, indicate whether it would appear in the operating, investing, or financing section of the statement of cash flows (in $ thousands).

a. Member distributions (dividends) $(11,599)

b. Net income 6,543

c. Payments on revolving credit facility (4,900)

d. Purchases of marketable securities (5,671)

e. Depreciation expense 10,444

f. Accounts payable 705

g. Proceeds from issuance of Class B common stock 45

h. Equity-based compensation 14,488

i. Inventories (45)

j. Purchases of property and equipment (40,007)

Answers

Answer:

a. financing

b. operating

c. operating

d. investing

e. operating

f. operating

g. financing

h. no effect

i. operating

j. investing

Explanation:

Operating Section :

Include items that generate cash through trading operations in the course of business.

Investing Section :

Include items that generate cash through disposal or acquisition of tangible and intangible assets including financial assets.

Financing Section :

Include items that generate cash through investment by owners, lenders and repayments of their capital thereof.

The December 31, 2018, adjusted trial balance for Fightin' Blue Hens Corporation is presented below.

Accounts Debit Credit

Cash $12,000

Accounts Receivable 150,000

Prepaid Rent 6,000

Supplies 30,000

Equipment 400,000

Accumulated Depreciation $135,000

Accounts Payable 12,000

Salaries Payable 11,000

Interest Payable 5,000

Notes Payable (due in two years) 40,000

Common Stock 300,000

Retained Earnings 60,000

Service Revenue 500,000

Salaries Expense 400,000

Rent Expense 20,000

Depreciation Expense 40,000

Interest Expense 5,000

Totals $1,063,000 $1,063,000

Accounts Debit Credit

Service Revenue 500,000

Salaries Expense 400,000

Rent Expense 20,000

Depreciation Expense 40,000

Interest Expense 5,000

Total $1,063,000 $1,063,000

Required:

1. Prepare an income statement for the year ended December 31, 2021.

2. Prepare a statement of stockholders' equity for the year ended December 31, 2021, assuming no common stock was issued during 2021.

3. Prepare a classified balance sheet as of December 31, 2021.

Answers

Answer:

Please see answers below

Explanation:

1. Prepare an income statement for the year ended, December 31, 2021

Fightin' Blue Hems Corporation, Income statement for the year ended, December 31, 2021.

Details

$

Service revenue

500,000

Salaries expense

400,000)

Rent expense

20,000)

Depreciation expense

40,000)

Interest expense

5,000)

Earnings for the year

35,000

2. Prepare a statement of stockholder's equity for the year ended, 31, December, 2021

Fightin' Blue Hens Corporation statement of stockholder equity for the year ended , December 31, 2021.

Details

$

Common stock

300,000

Retained earnings

60,000

Earnings for the year

35,000

Stockholder equity

395,000

3. Prepare a classified balance sheet as at 31, December

Fightin' Blue Hens Corporation, classified balance sheet for the hear ends, December 31, 2021.

Details

$

Fixed assets

Equipment

400,000

Accumulated depreciation

135,000

Net fixed assets

265,000

Current assets

Cash

12,000

Accounts receivables

150,000

Prepaid rent

6,000

Supplies

30,000

Total current assets

198,000

Current liabilities

Accounts payable

($12,000)

Salaries payable

(11,000)

Interest payable

(5,000)

Working capital

170,000

Long term liabilities

Notes payable (due in two years)

(40,000)

Net total assets

395,000

Financed by;

Common stock

300,000

Retained earnings

60,000

Earnings for the year

35,000

Stockholder equity

395,000

Alice and Bob entered into a forward contract some time ago. Alice has the long position, while Bob has the short position. The forward contract will mature in three months and has a delivery price of $40. The current forward price for the contract is $42. The three-month risk-free interest rate (with continuous compounding) is 8%. What is the value Bob's position?

Answers

Answer:

$ - 1.96

Explanation:

After three months, Alice (long the contract) can buy the underlying by paying the delivery price of $40 which is $2 less than $42 the long position would have to pay if the contract was entered today.

DATA

Delivery price = $40

The three-month risk-free interest rate (with continuous compounding) =8%.

The current forward price = $42

Solution

So based on the present situation, Alice would be in $2 profit at the end of 3 months and Bob would be in $2 loss

Present value of Bob's loss (with continuous compounding) = 2\times e^{-0.08\times 0.25}

Present value of Bob's loss (with continuous compounding) = $1.96

The value of Bob's position is $ - 1.96

QUESTION 2 / 10

Which of the following is the BEST reason to use cash for making purchases?

A. Keeping track of how much you have spent is simple.

B. Splitting bills with friends is easier.

C. Getting more cash from an ATM machine is easy to do.

D. Knowing what you have spent your money on is

simple.

Answers

The best reason to use cash for making purchases is keeping track of how much you have spent is simple. Thus, option A is correct.

What is purchases?Purchasing is the process through which a company or organization acquires products or services in order to achieve its objectives. Although numerous organizations seek to establish standards in the purchasing process, practices can vary widely amongst firms.

Cash makes budgeting and sticking to it simpler. When you pay with cash that you've planned for purchases, it's easy to keep track of where your money is going. It's also eye-opening and keeps you grounded in terms of how much money is going out vs coming in from week to week or month to month.

The main incentive to utilize cash for purchases is that it is simple to keep account of the amount you have spent. As a result, option A is correct.

Learn more about purchases here:

https://brainly.com/question/24112214

#SPJ2

Lemon Corporation generated $324,600 of income from ordinary business operations. It also sold several assets during the year. Compute Lemon’s taxable income under each of the following alternative assumptions about the tax consequences of the asset sales.

a. Lemon recognized a $5,500 capital gain and a $7,400 net Section 1231 loss.

b. Lemon recognized a $6,500 capital loss and a $4,700 net Section 1231 gain.

c. Lemon recognized a $2,500 capital gain, a $3,900 capital loss, and a $3,000 net Section 1231 gain.

d.Lemon recognized $4,000 of depreciation recapture, a $2,000 Section 1231 gain, and a $4,200 Section 1231 loss.

Answers

Answer:

a. Lemon’s taxable income = $322,700

b. Lemon’s taxable income = $324,600

c. Lemon’s taxable income = $326,200

d. Lemon’s taxable income = $326,400

Explanation:

Before the questions are answered, the provisions of section 1231 of the Internal Revenue Service (IRS) rules are quoted as follows:

- If you have a net section 1231 loss, it is an ordinary loss.

- If you have a net section 1231 gain, it is ordinary income up to the amount of your unrecaptured section 1231 losses from previous years. The rest, if any, is a long-term capital gain.

Therefore, net section 1231 loss which is an ordinary loss is deducted from ordinary business operations to obtain taxable income.

Also, we describe the following:

Taxable income can be described as the amount of income that is employed to calculated the amount of tax that is payable to the government by an individual or a company in a particular tax year. It is obtained after making all required additions and allowable deductions.

Capital gain can be described as an increase in the value of a capital asset which is realized when the asset is sold. For tax purposes, capital gain is added to the income from ordinary business operations to obtain taxable income.

Capital loss can be described as a decrease in the value of a capital asset which is recognised when the asset is sold. For tax purposes, capital loss is deducted from the income from ordinary business operations to obtain taxable income.

We therefore proceed as follows:

a. Lemon recognized a $5,500 capital gain and a $7,400 net Section 1231 loss.

From the question, we have the following:

Income from ordinary business operations = $324,600

Capital gain recognised = $5,500

Net Section 1231 loss recognised = $7,400

Based on the explanation provided above, Lemon’s taxable income under this scenario is therefore calculated as follows:

Lemon’s taxable income = Income from ordinary business operations + Capital gain recognised - Net Section 1231 loss recognised = $324,600 + $5,500 - $7,400 = $322,700

b. Lemon recognized a $6,500 capital loss and a $4,700 net Section 1231 gain.

From the question, there is nothing related past five years stated and it is therefore assumed that there is no net section 1231 loss in the past five years.

As result, the total of $4,700 net Section 1231 gain is regarded as a capital gain and it is set-off against the $6,500 capital loss as follows to obtain the non-deductible expense as follows:

Non-deductible expense = $6,500 - $4,700 = $1,800

Since there is nothing deductible again, Lemon’s taxable income under this scenario is therefore equal to the income from ordinary business operations of $324,600. That is,

Lemon’s taxable income = $324,600

c. Lemon recognized a $2,500 capital gain, a $3,900 capital loss, and a $3,000 net Section 1231 gain.

Since no net section 1231 loss in the past five years is indicated here, the $3,000 net Section 1231 gain will be treated as a long-term capital gain.

Based on the provisions of section 1231 of the Internal Revenue Service (IRS) rules quoted above, non-deductible expense is calculated by deducting the $3,900 capital loss to the extent of the $2,500 capital gain as follows:

Non-deductible expense = $3,900 - $2,500 = $1,400

Since the $3,000 net Section 1231 gain has to be treated as a long-term capital gain, the $1,400 will be deducted from it obtain the net capital gain as follows:

Net capital gain = $3000 - $1400 = $1600

Lemon’s taxable income under this scenario is therefore calculated by adding the $1,600 net capital gain to the $324,600 income from ordinary business operations as follows:

Lemon’s taxable income = $324,600 + $1600 = $326,200

d. Lemon recognized $4,000 of depreciation recapture, a $2,000 Section 1231 gain, and a $4,200 Section 1231 loss.

We have the following:

Section 1231 loss = $4,200

Section 1231 gain = $2,000

Therefore, we have:

Net section 1231 loss = Section 1231 loss - Section 1231 gain = $4,200 - 2,000 = $2,200

This net section 1231 loss of $2,200 is therefore treated as ordinary loss as already stated in the provisions of section 1231 of the Internal Revenue Service (IRS) rules quoted above and deducted from the $324,600 income from ordinary business operations.

In addition, the depreciation recapture of $4,000 will be treated as ordinary income and it will be added to the $324,600 income from ordinary business operations.

Lemon’s taxable income under this scenario is therefore calculated as follows:

Lemon’s taxable income = Income from ordinary business operations + Depreciation recapture - Net section 1231 loss = $324,600 + $4,000 - $2,200 = $326,400

Thirteen students entered the business program at Sante Fe College 2 years ago. The following table indicates what each student scored on the high school SAT math exam and their grade-point averages (GPAs) after students were in the Sante Fe program for 2 years.

Student A B C D E F G

SAT Score 421 375 585 693 608 392 418

GPA 2.93 2.87 3.03 3.42 3.66 2.91 2.12

Student H I J K L M

SAT Score 484 725 506 613 706 366

GPA 2.50 3.24 1.97 2.73 3.88 1.58

The least-squares regression equation that shows the best relationship between GPA and the SAT score is:________ (round your responses to four decimal places)

Answers

Answer:

ŷ = 0.0035X + 1.0030

Explanation:

Given the data :

Student A B C D E F G H I J K L M

SAT Score: 421 375 585 693 608 392 418 484 725 506 613 706 366

GPA: 2.93 2.87 3.03 3.42 3.66 2.91 2.12 2.50 3.24 1.97 2.73 3.88 1.58

We can obtain the Least square regression calculator, we can obtain the least square regression equation in the Format :

y = mx + c

Where ; m = gradient / slope

x = predictor variable ; c = intercept

y = Independent variable.

The model equation produced by the calculator is :

ŷ = 0.0035X + 1.0030

y predicted variable ; x = explanatory variable

0.0035 = slope or gradient ; 1.0030 = intercept

Find out more information about sat score here:

https://brainly.com/question/2264831

definition of observant in entrepreneur characteristics

Answers

Answer:

In Entrepreneur characteristics, observant refers to the ability to quickly notice a certain pattern or unusual situation.

This skill is important because of these two following reasons:

- It helped the entrepreneur notice an existing trend. This trend could represent the things that are currently favored by the consumers in a certain market. Understanding trend will help you creating a product that can fit into that trend.

- It also help the entrepreneur notice the problems that occur internally. For example, being observant will help the entrepreneur notice the negative emotion that the employees experience when facing a certain problem. After noticing this, the entrepreneur could develop some sort of strategy to lift their spirit.

BMW’s vehicle-assembly facility in South Carolina represents a direct investment inside the United States by the German manufacturer. This facility is an example of:

Answers

Answer:

Foreign direct investment.

Explanation:

BMW’s vehicle-assembly facility in South Carolina represents a direct investment inside the United States by the German manufacturer. This facility is an example of foreign direct investment.

A foreign direct investment (FDI) can be defined as an investment made by an individual or business entity (investor) into an investment market (industry) located in another country. The investor here, shares a different country of origin from the country where his investment is located.

In a foreign direct investment (FDI), an investor must establish his business, factory and operations in a foreign country or acquire assets in a business that is being operated in a foreign country.

Additionally, foreign direct investment (FDI) are categorized into three (3) main types and these are;

1. Vertical FDI: it involves establishing a different business that is however similar to the main business owned by the investor.

2. Horizontal FDI: it involves establishing the same type of business in a foreign country as owned in the investor's country.

3. Conglomerate FDI: it involves establishing a business that is completely different in another (foreign) country.